submitted by jwithrow.

Journal of a Wayward Philosopher

Individual Solutions: Building Financial Resiliency

February 12, 2015

Hot Springs, VA

The S&P opened at $2,071 today. Gold is down to $1,226 per ounce. Oil is floating around $49 per barrel. Bitcoin is hanging around $221 per BTC, and the 10-year Treasury rate opened at 2.03% today.

Ten central banks have cut interest rates so far in 2015. The list includes: Australia, Canada, China, Denmark, India, Egypt, Pakistan, Peru, Russia, and Turkey. Additionally, both the Bank of Japan and the European Central Bank are actively buying sovereign debt… with counterfeited currency created from thin air. The Federal Reserve is taking a break from this exercise after nearly six years of creating currency to shop at the U.S. Treasury and go yard-saling on Wall Street. Of course the $4.5 trillion worth of sovereign debt and mortgage-backed securities still sits on the Fed’s balance sheet in the interim.

All of this economic intervention is a concerted effort to stave off a major credit contraction. The central bankers talk about hitting certain GDP and unemployment rate metrics but that is all part of their dog and pony show. If creating currency out of thin air could actually grow an economy and create jobs then we would already live in a utopian paradise. But that’s just not how the world works.

Try as they may to avoid it, the coming credit contraction is inevitable. You see, the global monetary system has been fraudulent for a little more than four decades now. Gold officially anchored the global monetary system for two centuries prior to 1971. Then, in 1971, President Nixon’s administration acted to break away from two hundred years of tradition and the U.S. ended direct convertibility of the dollar to gold. Of course the “Great Society” welfare programs and the Vietnam War had a lot to do with this decision.

“Your dollar will be worth just as much tomorrow as it is today,” Nixon proclaimed on television with a straight face. “The effect of this action, in other words, will be to stabilize the dollar.”

Of course the exact opposite happened: the U.S. dollar fell off a cliff. Anyone living during the 70’s can attest to this. What was the price of a new home back then? A new car? A hamburger? The difference between what those items cost in 1971 and what they cost today represents how far the U.S. dollar has fallen in purchasing power.

How did this happen?

Well, with all ties to gold removed governments and central banks discovered they could conjure currency into existence to pay for anything they wanted. Tanks, fighter jets, food stamps, Medicare part D, $800 trash cans… no problem! So they embarked upon this historic credit expansion armed with a magical monetary system that provided them with money for nothing.

But governments weren’t the only beneficiaries. The companies making the tanks and the bombs made out like bandits. So did all of the bureaucrats who were hired as government expanded. And the people receiving welfare benefits found the system quite palatable as well. Pretty soon smart people learned that the best business in the world was to sell something to the U.S. government because it had unlimited money to spend. So they descended upon K Street like buzzards on road-kill and pretty soon the suburbs surrounding D.C. claimed home to six of the wealthiest ten counties in the U.S.

The champagne has been flowing up on the Hill and in the lobbyist offices on K Street for four decades now thanks mostly to the fraudulent fiat monetary system in place since 1971. The establishment hails their elastic currency system as a major success but theirs is a self-serving and short term view. Credit has been constantly expanding since 1971 but do we really think this can go on forever? Can we continue to run up debt, print money to pay interest on that debt, and then buy all of the fighter jets, disability checks, politicians, and cheap junk from China without ever having to think twice about it? If not, what happens when the credit contracts and we can no longer afford all of these expenditures?

The Austrian School of Economics tells us what the result of this madness will be: a “crack-up boom” followed by a monstrous bust as all of the bad debt and malinvestments are finally liquidated.

The crack-up boom occurs as the prices of assets and real goods are driven up to the moon by enormous amounts of excess currency conjured into existence in an attempt to perpetuate the credit expansion. After all, that new currency has to go somewhere. This scheme will work to stave off the credit contraction… until it doesn’t. Then cometh the bust.

While Austrian Economics can make the diagnosis, the timing of the bust cannot be predicted. There are too many interconnected factors at play. What’s important is that there is still time to build financial resiliency in advance. The cornerstone of financial resiliency is knowledge and understanding. Understand fiat money is an illusion. Understand the difference between money and wealth. Study Austrian Economics to get a feel for what’s really going on in the economy.

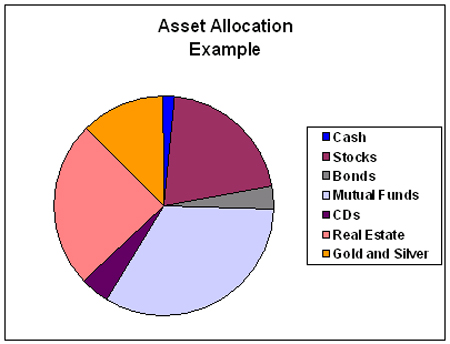

Once you understand how the monetary system actually works you can formulate a customized asset allocation model based upon your personal circumstances.

A resilient asset allocation model will consist of cash (20-30%), precious metals (10-30%), real estate (30-60%), and strategic equities (10-15%).

At minimum you should carry enough cash to cover at least 6-12 months of expenses. Distressed assets will go on sale when then bust hits so any cash in excess of your reserve fund can be used to acquire these distressed assets (real estate, stocks, businesses, etc.) when they are cheap.

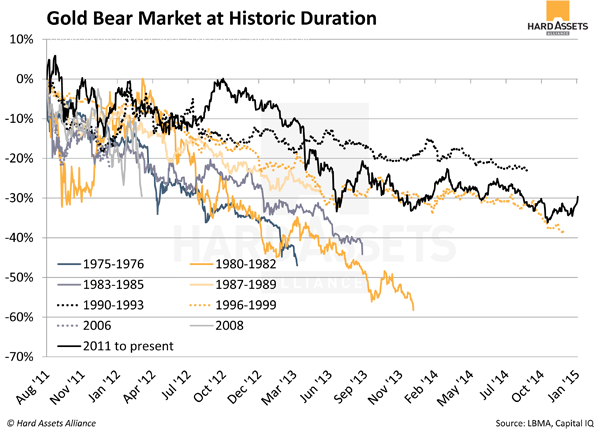

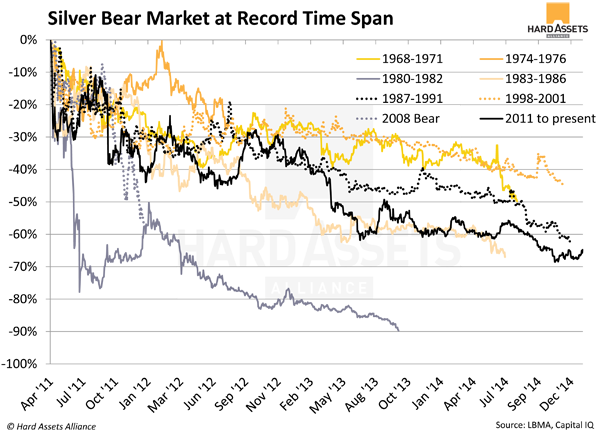

Your precious metals allocation should consist of physical gold and silver bullion stored at home or in a legal segregated account overseas. Never store precious metals in a domestic bank vault – Americans learned this the hard way back in the 30’s when the banks closed and FDR raided the vaults to confiscate gold. Remember, precious metals are insurance not speculation. The price of gold (and silver) will skyrocket in terms of fiat currency, but its purchasing power will remain relatively constant just as it has for thousands of years. Those who save in fiat currency will see their wealth evaporate as the credit contraction unfolds while those who hold precious metals will weather the storm. J.P Morgan testified before Congress in 1912: “Gold is money. Everything else is credit.” Don’t be fooled.

Real estate presents a unique opportunity currently as we are living during a period of historically low interest rates and lenders are willing to offer long term mortgages at these low rates. This provides a tremendous opportunity to lock in these low rates on real estate for thirty years during which time interest rates will inevitably rise significantly.

We firmly believe stocks should make up the smallest percentage of a resilient portfolio under current economic conditions. Stockholders have been the primary beneficiaries of the massive credit expansion and all of the easy-money chicanery over the past several years. Financial institutions have poured new money into the equities markets and publicly-traded companies have used a ton of excess cash to buy back shares of their own stock. As a result current stock valuations do not reflect the underlying health of the economy. Though stocks will run for a bit longer, we are closer to the end than the beginning of the bull cycle. We think the exception is in the resource and commodity sector, however. The stocks of well-managed companies in this sector could do extremely well over the next few years as the global financial system continues to falter.

Nobody can control macroeconomic conditions but we can each control our individual response to them. Building financial resiliency by constructing a diversified portfolio across several asset classes is an individual solution to a collective problem. Financial resiliency is just half of the picture, however. Tomorrow we will look at what we call home resiliency.

Until the morrow,

Joe Withrow

Wayward Philosopher

For more of Joe’s thoughts on the “Great Reset” and the paradigm shift underway please read “The Individual is Rising” which is available at http://www.theindividualisrising.com/. The book is also available on Amazon in both paperback and Kindle editions.