submitted by jwithrow.

Journal of a Wayward Philosopher

On the National Debt

October 7, 2014

Hot Springs, VA

The S&P is down to $1,953, gold is up to $1,212, oil is up to $89, bitcoin is up to $330, and the 10-year is down to 2.38%.

Looks like the 10-year Treasury rate is still well-corralled for the moment. And gold is still on sale.

Yesterday we examined a few of the traps cleverly hidden for infants coming into the world at this time – prompted by wife Rachel and my expectations of a little girl named Madison set to begin her journey here on Earth within the next few days or weeks. Today let’s look at the overt trap that boldly claims the right to little Madison’s future earnings: the national debt.

It is popular today for politicians to speak out against the national debt and boldly claim that ‘we’ (they love this ‘we’ business) need to balance the government’s budget and begin to pay the debt down. This sounds great and people will vote for you for making such a statement, but there are two problems this leaves unaddressed – one based in economics and one based in morality.

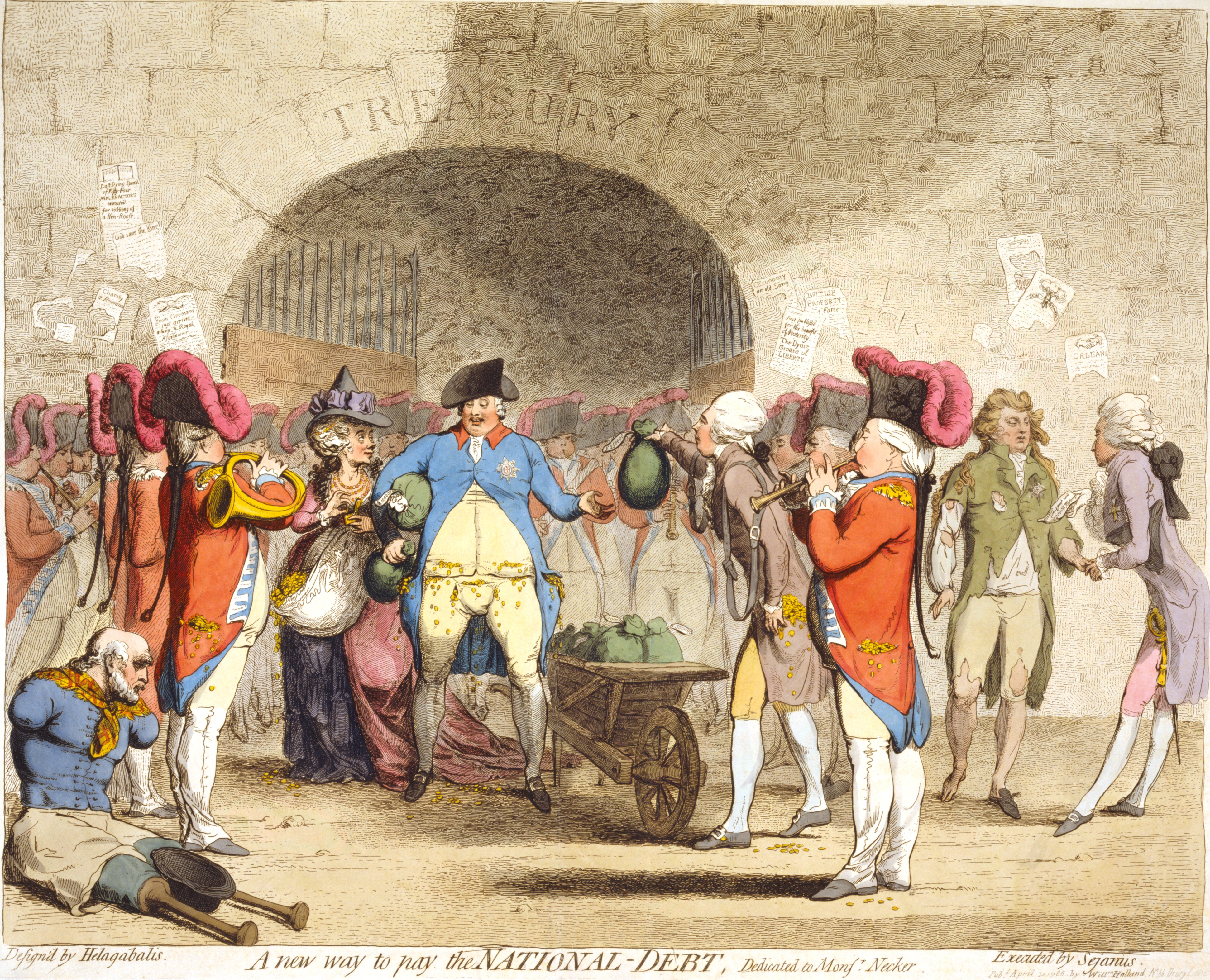

First, the economic problem: the national debt is not $17.75 trillion as advertised. The national debt is actually closer to $200 trillion if you calculate it according to generally accepted accounting principles (GAAP) which require you to record all future liabilities on your balance sheet. Most of these future liabilities that are not included in the official debt figure are Social Security and Medicare commitments. These future commitments are completely unfunded which means there exists no underlying revenue support and no asset backing. The only way these future commitments can be met is if enough money comes into the Social Security and Medicare programs versus going out. Demographics tell us that 10,000 Baby Boomers will retire EVERY SINGLE DAY for the next ten years, however, which suggests that a huge number of people are going to move from being contributors to these programs to recipients.

Oh, and both Social Security and Medicare already run annual deficits.

These politicians must be expecting quite a bit from my little Madison if they plan to balance the budget and pay down the debt with her future earnings.

But they don’t actually plan to balance the budget and pay down the debt. The simple fact is it can’t honestly be done without defaulting on the existing commitments in some capacity. There’s just too much debt and not enough production. Which leads us to the moral problem: this system is incredibly, unbelievably immoral.

Why should anyone be taxed and forced to pay for anything against their will? What kind of system assigns debt to infants from the moment they draw their first breath in this world? What kind of system incentivizes debt, dishonesty, consumption, and exploitation while punishing honesty and production?

My answer: a really bad one.

So did the economic problem lead to the moral problem or vice versa? I am not sure but history does suggest that dishonest fiat money seems to always undermine the morality and stability of society.

I will have more thoughts on that in a later entry. In the meantime be sure to order a copy of The Individual is Rising for a more in depth look at these economic problems, some financial strategies to prepare for the Great Reset, and more.

Focusing our attention back on the debt-trap: how best to prepare Maddie for life in a society that plans to confiscate her future earnings to pay for the immorality of earlier generations?

It is a shame that I have to spend any time at all on this question here in what is supposed to be the “Land of the Free”. The more I think about it, the more I become convinced that education is the key to preparing our children for the world that awaits them.

Not education of the public kind, however. It looks to me like the public schools are setting children up to be victims of the immoral System. The public school system fosters a herd mentality and requires students to subordinate themselves to “authority” at all times. Such an environment is not going to stimulate the creativity and self-confidence necessary to thrive in a society that expects the next generation to pay the debts of the previous. Instead, this method of education is going to condition students to happily embrace their servitude to the System as it pillages the fruits of their labor in the name of the “common good”.

Far better to create an individualized educational experience tailored to Madison’s unique skills and interests. Instead of forcing subjects upon her, why not let her guide her own education? Rachel and I will probably need to do most of the guiding in the early years, but I suspect Madison will be plenty capable of determining her own path as she grows and matures. Enabling self-education in this manner will certainly do a better job of preparing her for adult-hood than the government school system that conditions students to always seek guidance and permission from “experts” instead of trusting their own abilities.

Of course this self-education will need to be blended with social activities as well. Fortunately, one can find all manner of groups, clubs, and activities using a simple internet search these days so I don’t see this being much of a problem. What will Madison like to do? Dance? Aikido? Art? Music? Softball? All of the above?

The world will be her oyster…

More to come,

Joe Withrow

Wayward Philosopher

For more of Joe’s thoughts on the Great Reset and regaining individual sovereignty please read “The Individual is Rising” which is available at http://www.theindividualisrising.com. The book is also available on Amazon in both paperback and Kindle editions.