submitted by jwithrow.

Journal of a Wayward Philosopher

How to Insulate Your Portfolio from the Fed’s Financial Destruction

January 16, 2015

Hot Springs, VA

The S&P opened at $1,992 today. Gold is up to $1,267 per ounce. Oil is back down under $47 per barrel. Bitcoin is checking in at $210 per BTC, and the 10-year Treasury rate opened at 1.72% today. Famed Swiss economist Marc Faber went on record at a global strategy session this week saying he expected gold to go up significantly in 2015 – possibly even 30%.

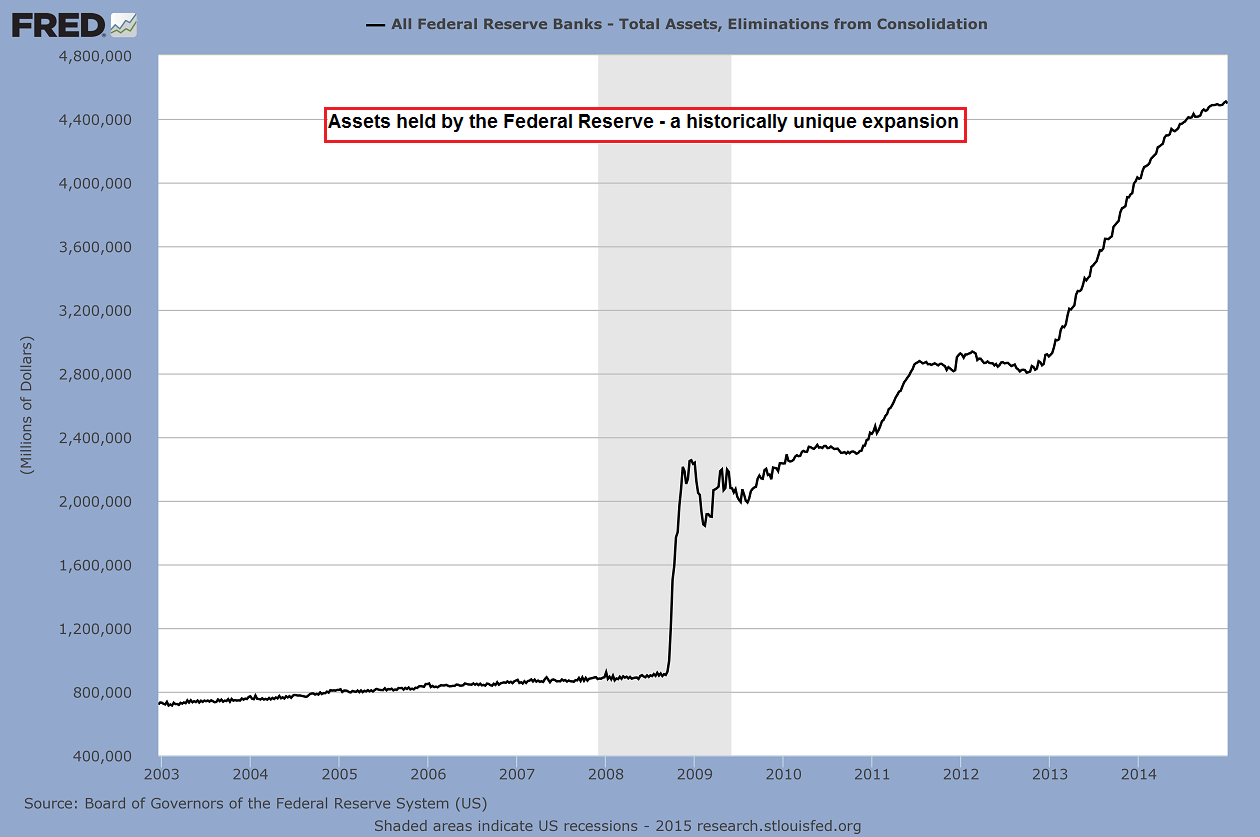

Yesterday we examined the Fed’s activity since 2007 and we noticed $3.61 trillion dollars sloshing around in the financial system that didn’t exist previously. Then we put two and two together and realized the answer was four… not five as the mainstream media claims. We came to the conclusion that the entire financial system is now dependent upon exponential credit creation out of thin air and that financial destruction cometh once the credit expansion stops.

Today let’s discuss some ideas for insulating our balance sheet from the ongoing financial crisis and the inevitable crack-up on the horizon.

The first and most important thing to understand is the difference between real money and fiat money. The Fed (and other central banks) issue fiat money at will – created from nothing. Dollars, euros, yen… none of them are real money; they are all fiat. These currencies do not represent real work, savings, or wealth and they certainly are not backed by anything of substance.

Most of these currencies exist as digital units out in cyberspace but if you read one of the paper notes in circulation it is completely honest with you:

”This note is legal tender for all debts, public and private.”

That means central bank notes are really good for paying debts but that’s about the extent of it.

All of these currencies depreciate over time in terms of purchasing power because they have no intrinsic value and their supply is unlimited. Even when a currency is “strong” as the U.S. dollar is currently, it is only strong measured against other currencies. Measure the dollar against your cost of living and you will see the real picture.

The point is we can’t trust central bank money.

Which leads us to the first way to insulate your portfolio from the Fed’s carnage: convert fiat money into real money – gold and silver. Gold and silver were demonetized in the late 60’s and early 70’s and the establishment has been downplaying their significance ever since. But there is a reason every central bank in the world still stockpiles gold. Gold and silver have been money for centuries and that is not going to change in a brief fifty year time span. Maybe one day cryptocurrencies will take the torch from gold and silver but that day is not today.

It is wise to maintain an asset allocation of 10-30% in physical gold and silver bullion. Precious metals will skyrocket in price measured against fiat currency as the Fed’s financial destruction plays out but in reality they are just a store of value. Precious metals will skyrocket in price only in terms of the fiat currency that is depreciating so dramatically.

Energy and commodity stocks, especially well managed resource companies, stand to boom as the monetary madness plays out as well. This is not a long-term strategy, however, so any gains captured during the commodity boom should be converted into hard assets or blue-chip equities after they have finished falling in price. There is enormous risk in the stock market so equities should make up a smaller portion of your asset allocation: 10-15% perhaps.

Despite everything said about fiat currency above, cash should still make up a large percentage of your portfolio; probably 20-30%. Cash loses purchasing power over time but it is still the primary medium of exchange so it is necessary to remain liquid. Ideally you should keep 6-12 months worth of reserve funds in cash and any cash above that threshold can be used to acquire assets as they go on sale. And plenty of assets will go on sale when the credit expansion stops.

The remainder of your asset allocation should be in real estate, provisions, other hard assets, and anything else that improves your quality of life. With all of the unjust systems and institutions to contend with it is easy to forget most of us are far richer than the wealthiest individuals living at the beginning of the 20th century. We have central heating and air in our homes, reliable auto travel over long distances, affordable air travel to anywhere in the world, way too much entertainment, cheap access to the internet which opens the door to all manner of information/commerce/entertainment, pocket-sized computers that double as telephones, and many other modern comforts that would be considered futuristic luxuries by the wealthiest of the wealthy one hundred years ago.

After properly aligning your portfolio to weather the Fed’s financial storm, focus on aligning your life to maximize fulfillment, purpose, and peace of mind. After all, your most valuable asset is time and time cannot be measured in financial terms.

More to come,

Joe Withrow

Wayward Philosopher

For more of Joe’s thoughts on the “Great Reset” and the fiat monetary system please read “The Individual is Rising” which is available at http://www.theindividualisrising.com/. The book is also available on Amazon in both paperback and Kindle editions.